Hong Kong SME Guide to Public Liability Insurance: Comprehensive Breakdown of Coverage, Premiums, and Common Misconceptions

- May 19

- 10 min read

For most bosses operating Small and Medium Enterprises (SMEs) in Hong Kong, the most worrying risk is not daily business losses, but a sudden third-party accident that can directly drag down the company and even implicate their personal assets.

Unlike mandatory Employees' Compensation (Labour) Insurance, the Hong Kong regulations do not have a statutory requirement for purchasing Public Liability (PL) insurance. However, the reality of doing business is much harsher: mall leases, government tenders, corporate partnerships, building entry requirements, and license renewals all strictly require a PL policy.

More crucially: Hong Kong is one of the cities with the highest claim amounts, most expensive legal fees, and strongest third-party rights awareness globally.

Data from the Hong Kong Federation of Insurers (HKFI) for 2026 shows:

Uninsured SMEs facing third-party claims pay an average compensation of up to HKD 820,000.

37% of uninsured enterprises go bankrupt due to a single accident, and 22% of bosses have to sell personal assets to pay for compensation.

Nearly 30% of SMEs buy the wrong insurance, under-insure, or make declaration errors, resulting in a 100% claim rejection when an incident occurs.

Public Liability Insurance (PL) covers: During business operations, any accident causing third-party (customers, pedestrians, tenants, partners, the public) bodily injury or property damage—covering the legally required compensation amount + full legal defense costs.

While Labour Insurance covers "employees," PL covers "outsiders." If you want to operate stably in Hong Kong and isolate your personal unlimited liability, PL is your first line of defense.

1. Core Concepts of Public Liability Insurance: Thoroughly Understanding "What is Covered and What is Not"

1.1 Core Coverage Scope (100% Standard Coverage) As long as it is an unintentional, non-illegal accident occurring during business operations, it is fully covered:

Third-Party Bodily Injury/Death: Customers slipping and fracturing bones, hot food scalds, equipment burns, falling object injuries, event accidents.

Third-Party Property Damage: Construction leaks flooding neighboring shops, signboards smashing vehicles, equipment dripping water damaging customer belongings.

Full Legal Fees: Litigation fees, lawyer fees, settlement fees, notarization fees, investigation fees, defense costs (even if the enterprise is not at fault, the insurance will fight the lawsuit for you).

Extendable Coverage: Food poisoning liability, leased premises damage liability, employee fieldwork third-party liability, advertising signboard liability.

1.2 Absolute Exclusions (Minefields for 90% of Enterprises) In the following scenarios, insurers have the legal right to reject claims; these are risks borne by the enterprise itself:

Employee injuries (Falls under Labour Insurance; PL does not cover).

Damage to the company's own goods, equipment, or renovations (Falls under Property Insurance).

Intentional acts by the enterprise, illegal operations, unlicensed operations, operating beyond the approved scope.

Professional service negligence (Consultation errors or beauty/medical mishaps require "Professional Indemnity Insurance").

War, riots, earthquakes, typhoons/extreme natural disasters, nuclear risks.

Concealing risks during application, falsely declaring the industry, hiding operational models.

2. PL Risk Data Comparison of 6 Mainstream SME Industries in Hong Kong (2026 Latest)

HK PL premiums do not have a flat rate. Industry attributes + operational scenarios + foot traffic density + risk level directly determine premiums, underwriting strictness, and claim success rates.

Industry Category | Risk Level | Annual Premium Range (HK$) | Recommended Min. Limit | Annual Claim Rate | Industry Rejection Rate | Underwriting Strictness |

Clerical / Consulting / IT Design | Low Risk | 1,500 – 3,500 | HK$ 10M | 5.8% | 1.2% | Lenient |

Retail / Stores / Offline E-commerce | Medium-Low Risk | 3,000 – 6,000 | HK$ 10M – 20M | 18.3% | 5.5% | Normal |

F&B / Cafes / Bakeries | Medium-High Risk | 6,000 – 15,000 | HK$ 20M – 30M | 35.7% | 16.8% | Moderately Strict |

Beauty / Nails / Fitness Services | Medium-High Risk | 5,000 – 12,000 | HK$ 20M – 30M | 24.5% | 11.3% | Moderately Strict |

Logistics / Delivery / Couriers | High Risk | 8,000 – 20,000 | HK$ 30M – 50M | 41.2% | 14.7% | Strict |

Renovation / Engineering / Cleaning | Ultra-High Risk | 12,000 – 30,000 | HK$ 50M – 100M | 48.9% | 23.5% | Extremely Strict |

Data Source: 2026 Hong Kong Federation of Insurers, QBE Underwriting Data, Annual Third-Party Claims Statistics

3. Industry-Specific Risk Analysis (Ultra-Detailed Pitfalls + Insurance Advice)

3.1 Clerical / Consulting / Design / IT Office (Low Risk)

Industry Scenarios: Purely indoor office, client visits/meetings, outdoor meetings, project surveys, fieldwork document delivery, no open flames, no high-risk equipment.

High-Frequency Claims:

Visitors tripping over wires or slipping on wet floors causing sprains/fractures.

Hanging cabinets, lighting, or shelves falling and hitting clients.

Hot water in the pantry scalding visitors.

Air-con leaks or office equipment leaks damaging client laptops/phones.

Employee traffic accidents during fieldwork involving third-party vehicles or pedestrians.

Biggest Hidden Risk: Many offices involve fieldwork or on-site services, but only declare "purely indoor clerical." If a fieldwork accident occurs, the policy rejects it directly.

Pitfall Avoidance:

As long as your office is open to client visits, PL must be purchased; otherwise, it violates the lease + leaves you without a safety net.

For fieldwork, on-site surveys, or events, you must proactively declare "fieldwork third-party liability."

Tidy up floor wires, keep reception areas dry, regularly check hanging items.

Insurance Config: Limit 10M, Deductible 5,000, must add fieldwork extension.

3.2 Retail / Storefronts / Convenience Stores / Boutiques (Medium-Low Risk)

Industry Scenarios: Dense foot traffic, customers freely entering/exiting, goods display, back-room warehouse, wet floors on rainy days, storefront hanging signboards.

High-Frequency Claims:

Customers slipping on muddy/wet floors brought in during rainy days.

Over-stacked shelves causing goods to fall and hit customers.

Glass doors or automatic doors pinching customers.

Exterior light boxes or signboards falling and hitting people/cars.

Staff pushing trolleys or moving goods and bumping into customers.

Biggest Hidden Risk: Declaring only "retail sales," while hiding the back warehouse, goods stacking, or outdoor displays. Claims are rejected due to "untruthful risk declaration."

Pitfall Avoidance:

Application must truthfully state: business area, whether there is a warehouse, whether there are outdoor displays, and types of goods.

Must have anti-slip warning signs on rainy days and retain floor-mopping inspection logs.

Limit shelf heights; inspect signboards and hanging fixtures monthly.

Insurance Config: Standard street shops 10M, busy mall shops 20M; must add signboard liability and property damage coverage.

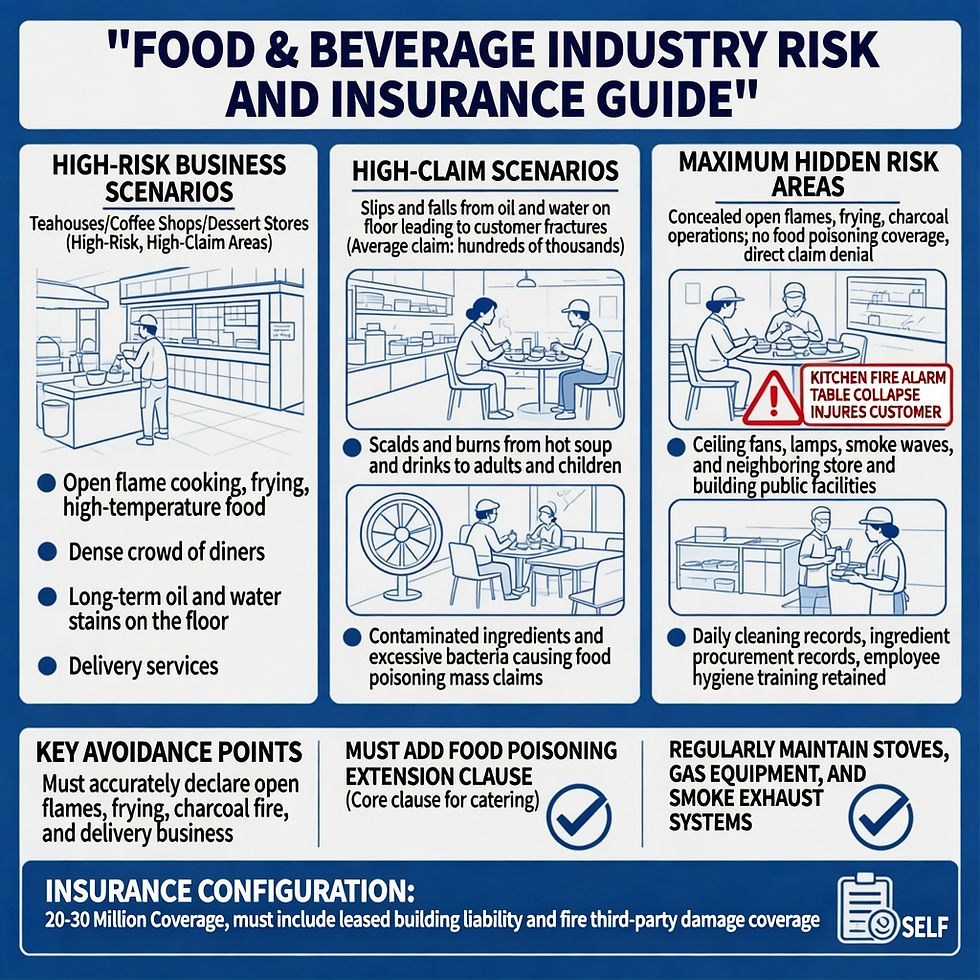

3.3 F&B / Cha Chaan Teng / Cafes / Dessert Shops (Medium-High Risk, High Claim Area)

Industry Scenarios: Open-flame cooking, deep-frying, hot food, dense dine-in traffic, floors with chronic grease/water stains, delivery services.

High-Frequency Claims:

Greasy/wet floors causing customer slips and fractures (single claims often reach hundreds of thousands).

Hot soup/drinks scalding adults or children.

Unclean ingredients/bacteria exceeding standards causing mass food poisoning claims.

Ceiling fans, lights, or dining chairs breaking and injuring diners.

Kitchen fires/smoke affecting neighboring shops and building public facilities.

Biggest Hidden Risk: Hiding open flames, deep-frying, or charcoal cooking; lacking the food poisoning extension clause, leading to direct rejection.

Pitfall Avoidance:

Must truthfully declare open flames, deep-frying, charcoal, and delivery business.

Must add Food Poisoning Extension Clause (the most core clause for F&B).

Retain daily cleaning logs, ingredient purchase records, and staff hygiene training records.

Regularly maintain stoves, gas equipment, and exhaust systems.

Insurance Config: 20M–30M limit; Leased premises liability and fire third-party damage coverage are mandatory.

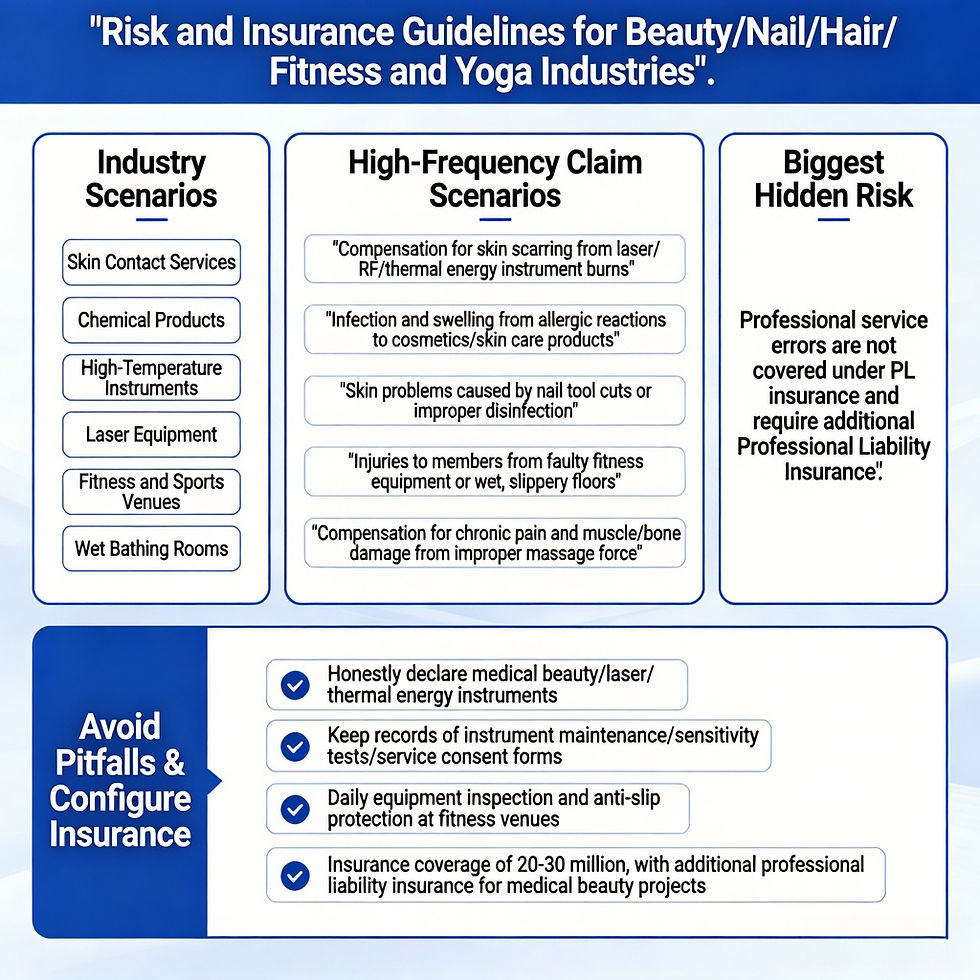

3.4 Beauty / Nails / Hair Salons / Fitness & Yoga (Medium-High Risk)

Industry Scenarios: Skin-contact services, chemical products, high-temperature equipment, laser equipment, fitness/sports areas, slippery shower rooms.

High-Frequency Claims:

Lasers, RF, or thermal equipment burning client skin or causing scars.

Cosmetics/skincare products causing allergies, swelling, or infections.

Nail tool cuts or improper sterilization causing skin issues.

Fitness equipment malfunction or wet floors causing member falls/strains.

Improper massage strength causing muscle/bone injury or chronic pain claims.

Biggest Hidden Risk: Assuming "professional service negligence" is covered by PL. PL actually does not cover professional mishaps; it must be paired with Professional Indemnity Insurance.

Pitfall Avoidance:

All medical beauty, laser, and thermal equipment must be truthfully declared.

Retain equipment maintenance logs, client sensitivity test records, and service consent forms.

Daily equipment checks and anti-slip treatments in fitness areas.

Insurance Config: 20M–30M; Medical beauty services must purchase additional Professional Indemnity Insurance.

3.5 Logistics / Courier / Delivery / Warehousing (High Risk)

Industry Scenarios: Vehicle fieldwork, street operations, mall/estate door-to-door deliveries, moving goods, warehouse stacking.

High-Frequency Claims:

Delivery vehicles colliding with pedestrians, third-party vehicles, or public facilities.

Falling goods during transit hitting pedestrians or damaging shops/vehicles.

Moving goods damaging mall elevators, hallway renovations, or glass facilities.

Warehouse goods collapsing and affecting neighboring third-party property.

Biggest Hidden Risk: Assuming Car Insurance can replace PL. Car insurance only covers traffic accidents; accidents during moving goods in public areas, falling goods, or facility damage rely solely on PL.

Pitfall Avoidance:

Policy must list all operating vehicles, service areas, and warehouse addresses.

Update the risk list immediately for newly hired deliverymen/drivers.

Standardize warehouse stacking and retain safety inspection logs.

Insurance Config: 30M–50M; must add vehicle operation third-party liability and elevator operation coverage.

3.6 Renovation / Engineering / Cleaning / Maintenance (Ultra-High Risk)

Industry Scenarios: Construction sites, work at heights, scaffolding, welding, wall demolition, drilling, exterior wall cleaning, building maintenance.

High-Frequency Claims:

Tools/materials falling from heights and hitting pedestrians or smashing vehicles.

Construction seepage/leaks flooding lower-floor residents or neighboring shop goods/renovations.

Welding sparks causing fires affecting building public areas.

Maintenance errors damaging power, water supply, or elevator facilities.

Biggest Hidden Risk: Concealing work at heights, welding, or demolition work; operating without certificates. 100% rejection if an accident occurs.

Pitfall Avoidance:

Work at heights, electrical work, and AC maintenance must be done by certified personnel; file the certificates.

Application must detail construction types, floor heights, and whether open flames are used.

Sites must have fences, warning tapes, and safety nets; retain daily safety logs.

Insurance Config: 50M–100M; must add water leakage liability and work at height third-party liability.

4. 2026 SME PL Insurance [Ultra-Detailed Cost-Saving Tips] (Legal, No Coverage Reduction, Practical Implementation)

Most SMEs overspend 25%–40% on unnecessary PL premiums annually. The core reasons: not understanding underwriting logic, buying blindly, not knowing how to apply for discounts, and failing to optimize risk levels. Below is the most complete and practical PL cost-saving system in the Hong Kong market for 2026.

4.1 Package Insurance Discounts (Biggest Single Saving: Average 20%–30%)

Principle: Single, low-priced policies are the most profitable for insurers; they are most willing to give concessions to "comprehensive clients." Buying PL alone yields no discounts, but bundling it with other insurance yields maximum benefits.

Best Combination: Employees' Compensation (Labour) Insurance + Public Liability Insurance + Corporate Property Insurance

Real Data:

Dual-Package (EC+PL): Average discount 15%–20%

Triple-Package (EC+PL+Property): Average discount 25%–32%

Steps:

Ask the same insurer for a unified quote before renewal.

Proactively inform the broker/insurer you are "willing to bundle all policies."

Request the package discount to be stated in writing to avoid empty verbal promises. Applicable to all industries; this is the most cost-effective saving method for SMEs.

4.2 NCB (No Claim Bonus) Accumulation Savings (Cheaper Every Year) Like Labour Insurance, PL has an official NCB tier system. Consecutive accident-free years can accumulate up to a 35% annual discount.

2026 Official NCB Tiers:

1 Year Zero Claims: 8%–15% Discount

2 Years Zero Claims: 15%–25% Discount

3+ Years Zero Claims: 25%–35% Max Discount

Core Strategy: For minor accidents under HKD 10,000, it is recommended to settle internally without claiming insurance. Once claimed, not only does your discount reset to zero, but next year's premium jumps by 10%–30%, far exceeding the repair/compensation cost.

Rule: Establish an "internal handling mechanism for minor losses" at the start of each year. Record the accident but do not file an insurance claim.

4.3 Precise Risk Declaration Savings (Resolving Overpayment for 90% of Enterprises) 90% of SMEs overpay because they declare too broadly or describe risks vaguely, leading the insurer to default to high-risk pricing.

Precise Tricks:

Zonal Declaration: Front shop is low-risk, back warehouse is medium-risk. Describe them separately so the whole area isn't charged at the high-risk rate.

Role Declaration: Clerical roles have no fieldwork, frontline roles have fieldwork. List them separately to avoid fieldwork surcharges for all staff.

Exclude Invalid Risks: Explicitly state if you have no work at heights, no open flames, or no mechanical operations to prevent default risk markups.

Result: Saves 12%–18% on average without affecting coverage or claims.

4.4 Reasonably Adjusting Deductible (Excess) to Lower Costs Deductible = The first amount you pay out of pocket when an accident occurs. The higher the deductible, the lower the insurer's risk, and the cheaper the premium.

2026 Market Golden Pairings:

Low-Risk (Clerical/IT): Deductible 5,000 → Raise to 10,000, Premium drops 10%–15%

Medium-Risk (Retail/Beauty): Deductible 10,000 → Raise to 15,000, Premium drops 12%–18%

High-Risk (F&B/Engineering): Deductible 20,000 → Raise to 30,000, Premium drops 15%–20%

Pitfall Avoidance: Do not blindly raise it too high. The core logic of "small amounts out-of-pocket, large amounts covered by insurance" provides the highest ROI.

4.5 Improve Corporate Safety Risk Control, Apply for Official Discounts (5%–15% Extra) Insurers are very willing to offer concessions to enterprises with "perfect safety management" due to extremely low accident rates.

Materials you can directly submit for discounts:

Staff safety training records.

Daily venue inspection and anti-slip cleaning logs.

Regular equipment maintenance and repair logs.

Proof of safety warning signs and protective equipment installation.

Data Proof: Enterprises with complete risk control files see a 42% drop in injuries and third-party accidents, and can apply directly to underwriting for an extra 5%–15% risk control discount.

4.6 Utilize 2026 Government SME Concessions + Tax Deductions (Hidden Savings) Compliant SMEs in Hong Kong enjoy dual benefits:

HKFI SME Comprehensive Insurance 15% Discount.

Premiums are fully tax-deductible as corporate operating costs.

After stacking tax benefits, actual insurance costs can drop by another roughly 10%.

4.7 Accurately Declare Business Scale to Avoid Inflated Premiums Some insurers price based on floating metrics like "turnover, floor area, and foot traffic." To make their policies look better, many companies overstate their turnover and scale, resulting in paying higher premiums for nothing.

Correct Approach: Declare true floor area, true headcount, and true operational models. Do not under-report, but do not exaggerate. This saves 8%–12% in wasted premiums annually.

5. PL Claim Failure Data Analysis & Standard SOP

Core Reason for Claim Failure | Percentage | Solution Strategy |

Missing Evidence, No Scene Records | 42.3% | Take photos/videos immediately; retain witnesses. |

Not Reported Within 24 Hours | 25.7% | Establish a 24-hour reporting mechanism. |

Untruthful Risk Declaration | 18.5% | Declare 100% truthfully during application. |

Incomplete Materials, Lost Receipts | 10.2% | Centrally file all medical/repair receipts. |

Rule Violations, Uncertified Operation | 3.3% | Ensure certified operation for high-risk roles. |

6. Annual Management Summary for HR/Bosses (5 Core Principles to Follow)

Don't leave it to chance: As long as you are open to the public, PL insurance is mandatory.

Don't conceal: Truthful risk declaration is the first prerequisite for a valid claim.

Save smartly: Rely on bundled packages, NCB accumulation, and risk control optimization to steadily reduce costs yearly.

Know your configuration: Match coverage limits to industry risks; avoid low-price traps and blind over-purchasing.

Standardize: Turn accident evidence collection, reporting, and material filing into strict SOPs to eliminate claim rejections.

Comments