Professional Liability (Professional Indemnity) Insurance in Hong Kong: A Comprehensive Report

- Aug 29, 2025

- 6 min read

Updated: Oct 9, 2025

Professional liability or Professional Indemnity insurance, commonly referred to as professional indemnity insurance (PII) in Hong Kong, is a type of coverage designed to protect professionals and businesses from financial losses arising from claims of negligence, errors, omissions, or breaches of duty in the provision of professional services.

It typically covers legal defense costs, settlements, and damages awarded to third parties. In Hong Kong, PII is essential for service-based industries due to the territory's common law system, which emphasizes accountability for professional misconduct.

The insurance market in Hong Kong is regulated and has seen steady growth, with the overall insurance sector projected to reach US$93.55 billion in gross written premiums by 2029, driven by economic recovery and increased awareness of risk management. This report examines regulations, professions involved, product features, premium factors, trends, and comparisons with other countries.

This report explores the relevant regulations, related professions, product features, premium factors, trends, and comparisons with other countries regarding professional liability insurance. For a more basic and detailed understanding of Hong Kong's professional liability insurance, please refer to: PROFESSIONAL INDEMNITY INSURANCE: COVERAGE, BENEFITS, COST, EXCLUSION, CLAIMS.

Regulations on Professional Liability (Professional Indemnity) Insurance

The Insurance Authority (IA) in Hong Kong, as an independent statutory body, is responsible for supervising insurance business, including Professional Indemnity Insurance (PII). The primary regulations are set out in the Insurance Ordinance (Cap. 41) and its subsidiary legislation, which stipulates that insurance brokers must maintain PII. It mandates that the minimum indemnity limit for brokers must not be lower than the amount determined by a specific formula, and the deductible must not exceed a specified limit, effective from January 1, 2024.

In addition to insurance brokers, several professional fields in Hong Kong also require or recommend practitioners to purchase professional indemnity insurance to protect against the risk of client losses due to professional negligence or errors. For example:

Lawyers: Governed by the Legal Practitioners (Professional Indemnity) Rules (Cap. 159M), they must participate in the Law Society of Hong Kong's Professional Indemnity Scheme (PIS) to provide indemnity for civil liability in practice.

Accountants: The Hong Kong Institute of Certified Public Accountants recommends that members purchase PII to address potential claims arising from negligence in auditing, taxation, or other accounting services.

Architects, Engineers, and Surveyors: Professionals engaged in architectural design, engineering consulting, or surveying in Hong Kong typically need to purchase PII to protect against losses resulting from design defects, construction errors, etc.

Doctors and Other Medical Professionals: Although there are no regulations in Hong Kong that mandate doctors to purchase PII, medical professionals typically purchase this type of insurance to address medical negligence claims.

Real Estate Agents: The Estate Agents Authority recommends that real estate agents purchase PII to protect against the risk of client losses that may result from providing incorrect information or negligence.

Other Professionals: Such as IT consultants, management consultants, education consultants, etc., may also need to purchase PII based on the nature and risk level of their profession.

These professional indemnity insurance requirements or recommendations are intended to protect the public interest and ensure that professionals are accountable for their actions, thereby maintaining the professional standards and reputation of the industry.

Different Professions

PII is crucial across various professions in Hong Kong, with some requiring mandatory coverage by law or professional bodies. The following table lists key professions, indicating whether coverage is compulsory and typical risks covered, along with approximate annual premium ranges based on available market data and general industry estimates (premiums vary by coverage limits, firm size, claims history, and insurer; figures are indicative and in HKD for standard individual or small firm policies with limits of HK$5-20 million):

Profession | Mandatory? | Key Risks Covered | Examples of Regulatory Bodies | Approximate Annual Premium Range (HKD) |

Solicitors/Lawyers | Yes | Civil liabilities from practice, negligence | The Law Society of Hong Kong | 5,000 - 50,000+ (depending on firm size and contributions under PIS) |

Accountants | Often required by regulators | Errors in financial advice, breach of duty | Hong Kong Institute of Certified Public Accountants | 3,000 - 15,000 (for master policy coverage) |

Architects/Engineers | Yes for regulated practices | Design flaws, project delays | Architects Registration Board, Hong Kong Institution of Engineers | 4,000 - 20,000 (higher for construction risks) |

Doctors/Healthcare Practitioners | Recommended, often mandatory via associations | Medical negligence, misdiagnosis | Medical Council of Hong Kong | 10,000 - 100,000+ (malpractice-specific, varies by specialty) |

Insurance Brokers | Yes | Negligent advice on policies | Insurance Authority | 3,000 - 12,000 |

Real Estate Agents | Recommended, sometimes required | Misrepresentation in property deals | Estate Agents Authority | 2,000 - 10,000 |

Counselors | Yes for association members | Breach of confidentiality, poor advice | Hong Kong Professional Counselling Association | 1,000 - 3,000 (e.g., HK$2,100 for HK$23M limit) |

Fitness Trainers/Consultants | No, but advisable | Injury claims from advice | N/A | 500 - 5,000 (e.g., similar to low-risk consultants) |

These professions are highly regulated, and PII ensures protection against claims that could arise from professional services. For instance, construction professionals increasingly obtain PII due to rising litigation in Hong Kong.

Product Features of Professional Indemnity Insurance

PII policies in Hong Kong offer broad coverage but with specific features and exclusions. Typical features include:

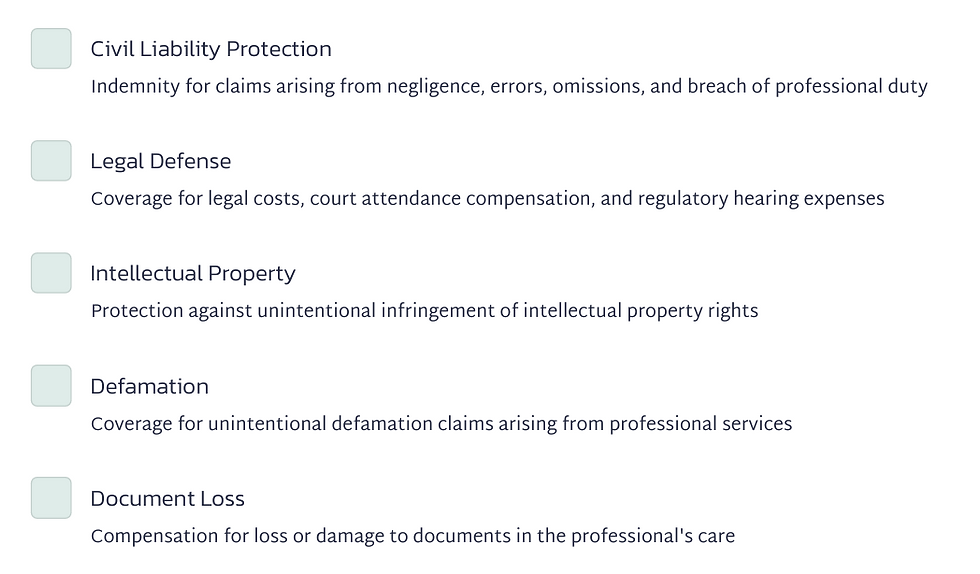

Core Coverage: Indemnity for civil liabilities, including negligence, errors, omissions, breach of duty, unintentional defamation, infringement of intellectual property, and loss of documents. Policies often cover defense costs, court attendance compensation, and regulatory hearing expenses.

Extensions: Some policies include bodily injury/property damage from professional services, automatic reinstatement of limits, and worldwide coverage (excluding high-risk jurisdictions like the USA/Canada unless specified).

Limits and Deductibles: Minimum limits vary by profession (e.g., HK$1 million or more for solicitors), with deductibles capped to ensure affordability.

Exclusions: Intentional acts, fraud, bodily injury/property damage (unless extended), and claims from non-professional activities. Policies are claims-made, requiring incidents to be reported during the policy period.

Additional Benefits: Run-off cover for retired professionals and compensation for settlements.

Policies from insurers like AIG, Chubb, and Allied World emphasize flexibility for SMEs and large firms.

Premium Factors

Premiums for PII in Hong Kong are influenced by several risk-based factors:

Profession and Risk Level: High-risk fields like medicine or law attract higher premiums due to litigation potential.

Claims History: Firms with prior claims face loadings; exceeding 50% of premiums in recent years can increase rates.

Coverage Limits and Scope: Higher limits or broader extensions (e.g., cyber risks) raise costs.

Business Size and Revenue: Larger firms or those with higher turnover pay more, as exposure increases.

Location and Jurisdiction: Worldwide coverage, especially including litigious areas, impacts premiums.

Market Conditions: Economic factors, regulatory changes, and insurer capacity affect rates, with hardening markets leading to exclusions.

Other elements include technology use (e.g., BIM in construction) and legal issues.

Premium Trends

From 2020 to 2025, Hong Kong's general insurance market, including PII, has shown resilience with gross written premiums growing from approximately HK$70 billion in 2020 to projected HK$85 billion by 2025, amid post-pandemic recovery. PII premiums have trended upward due to increased claims from regulatory scrutiny and economic pressures, with a hardening market noted in 2023-2024, leading to higher rates and exclusions.

Global influences, such as AI-driven risks and cyber threats, have pushed premiums higher, with Asia-Pacific PII demand growing. In Hong Kong, Q1 2025 saw total insurance premiums at HK$221 billion, up 43% year-on-year, indicating continued growth.

However, softening in management liability lines suggests potential stabilization by late 2025. Overall, premiums are expected to rise at 2-3% annually through 2029, driven by regulatory enhancements and business expansion.

Comparison with Other Countries

Hong Kong's PII framework shares similarities with common law jurisdictions but differs in compulsoriness, market size, and litigation culture. The table below compares key aspects with the UK, USA, Singapore, and Australia:

Aspect | Hong Kong | UK | USA | Singapore | Australia |

Regulatory Body | Insurance Authority (IA) | Prudential Regulation Authority/Solicitors Regulation Authority | State-level regulators (e.g., NAIC) | Monetary Authority of Singapore | Australian Prudential Regulation Authority |

Compulsory for Professions | Yes for lawyers, brokers; recommended for others | Yes for solicitors, accountants; sector-specific | Varies by state; often required for lawyers, doctors | Not always compulsory; mandatory for certain firms | Compulsory in states for lawyers; profession-specific |

Coverage Scope | Broad civil liability; excludes USA/Canada often | Similar; claims-made basis | Errors & Omissions; highly litigious, higher limits | Focus on negligence; evolving with AI risks | Comprehensive; includes fitness for purpose extensions |

Premium Levels | Moderate; influenced by small market size | Higher due to soft market cycle | Highest; driven by lawsuits | Competitive; growing demand | Varies; hardening for high-risk |

Market Trends | Growth amid regulation; hardening 2023-2025 | Softening with increased capacity | Stable but volatile in claims | Increased awareness post-pandemic | Mandatory schemes; AI impacts rising |

Key Differences | Compulsory schemes like PIS for public protection | More mature market; EU influences | Excludes from many international policies due to risks | Regional hub; less litigious than HK | State variations; compulsory for bars |

Hong Kong's system is more centralized and compulsory-focused compared to Singapore's flexible approach, while differing from the USA's fragmented, high-cost model.

Conclusion

Professional liability insurance in Hong Kong plays a vital role in safeguarding professionals against evolving risks, supported by robust regulations and a growing market. While premiums are influenced by profession-specific factors and show upward trends, comparisons highlight Hong Kong's balance between compulsion and flexibility relative to peers.

Established in 2014 as a Hong Kong-based leader, EverBright specializes in actuarial consulting and brokerage, designing and placing tailored liability insurance plans to optimize coverage and costs. With partnerships with global insurers, we provide innovative services in regulatory compliance, financial reporting, and more, making them an ideal partner for navigating the complexities of PII in various sectors.

Comments